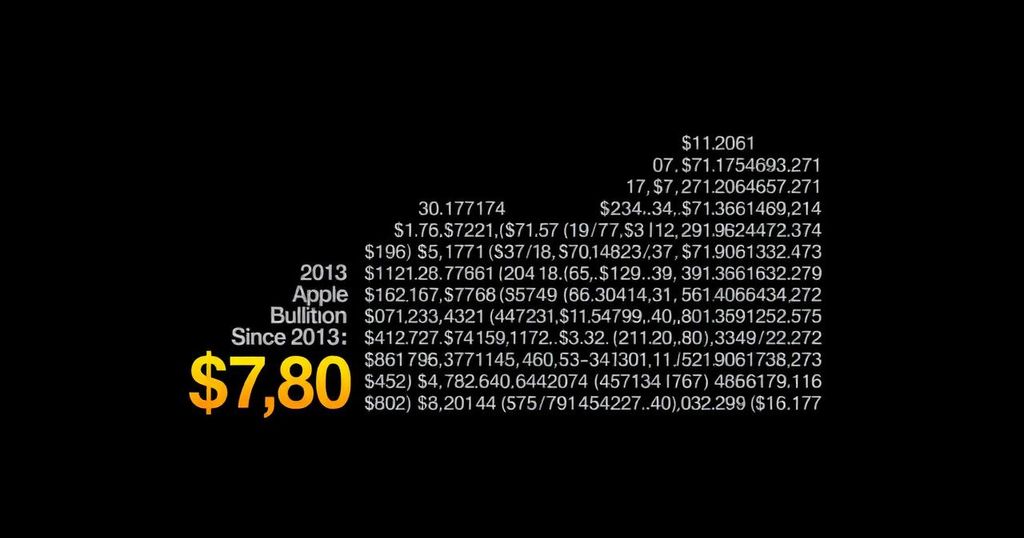

Apple Inc. has achieved a remarkable $3 trillion valuation but faces significant challenges with growth stagnation in its product segments. Despite a significant $700 billion investment in share repurchases that has benefitted shareholders through boosted earnings per share, the company’s core hardware sales, particularly the iPhone, have plummeted. Consequently, Apple’s financial maneuvers cannot mask the more profound growth issues it currently encounters, raising questions about its long-term sustainability and market valuation.

In recent years, Apple Inc. has maintained its status as a dominant force in the technology industry, becoming the first public company to achieve a $3 trillion market capitalization in June 2023, following its inaugural $1 trillion market cap in August 2018. Despite this monumental success and a staggering investment of approximately $700 billion in share repurchases since 2013, the company faces its most significant challenge yet: stagnating growth in its product segments. Apple’s considerable investment strategy has undeniably benefited its shareholders. Warren Buffett, CEO of Berkshire Hathaway, made Apple his top holding, citing the company’s extensive competitive advantages. Apple’s branding remains unparalleled, having secured the title of the world’s most valuable brand in Kantar’s “BrandZ Most Valuable Global Brands Report” for 2024, being the only company valued at over $1 trillion. The iPhone, which generates over half of Apple’s net sales, sustains remarkable market share dominance, holding more than 50% of the U.S. smartphone market. Beyond hardware, Apple under the leadership of CEO Tim Cook is also expanding its Services segment, which has witnessed significant revenue growth. The firm has invested heavily in share repurchases, with a breakdown revealing that the program has reduced Apple’s share count by over 42% since its peak. This strategic buyback program has elevated earnings per share (EPS) significantly, making the stock more attractive to value-oriented investors. The absence of buybacks would have resulted in a considerably lower trailing twelve-month EPS. Conversely, the company’s growth rates have faltered in recent years. Despite significant revenue from Services, Apple’s physical product lines, particularly the iPhone, have shown signs of sluggishness, with sales decreasing by 1% compared to the previous year. The lack of groundbreaking innovations in newer iPhone models has left consumers unimpressed. Similarly, sales declines have been witnessed across other segments such as iPads and wearables. The overall growth in revenue is minimal, climbing only 1% over the last year, and net income has stagnated, reinforcing the severity of the growth issue facing Apple. In a period characterized by significant inflation and market volatility, Apple’s valuation appears uncharacteristically high at 31 times estimated earnings for the forthcoming year, indicating a troubling disconnect between valuation and operational performance.

Apple Inc., an entity synonymous with innovation and market leadership in the technology sector, has navigated both explosive growth and considerable challenges over the past decade. The company’s ascendance to a $3 trillion valuation is underscored by notable endeavors in share repurchasing, designed to enhance shareholder value. Despite the ingenious branding and a stronghold on the smartphone market, Apple confronts a pressing dilemma: the stagnation of growth in its core product segments poses a risk that cannot be mitigated merely through financial maneuvers.

In summary, while Apple’s investment in share repurchases has undeniably bolstered earnings and shareholder value, it has not addressed the more pressing issue of revenue stagnation across its product lines. The company’s extraordinary valuation amid declining growth metrics calls for a re-evaluation of its strategies moving forward. Without substantial innovation and growth in revenue streams, Apple’s market position may become increasingly tenuous, despite its strong brand loyalty and established market presence.

Original Source: www.fool.com

Leave a Reply